Genres/Tags: Action, Fantasy, Shooter, First-person, 3D

Companies: Flying Wild Hog, Devolver Digital

Languages: RUS/ENG/MULTI11

Original Size: 23.1 GB

Repack Size: from 15.2 GB [Selective Download]

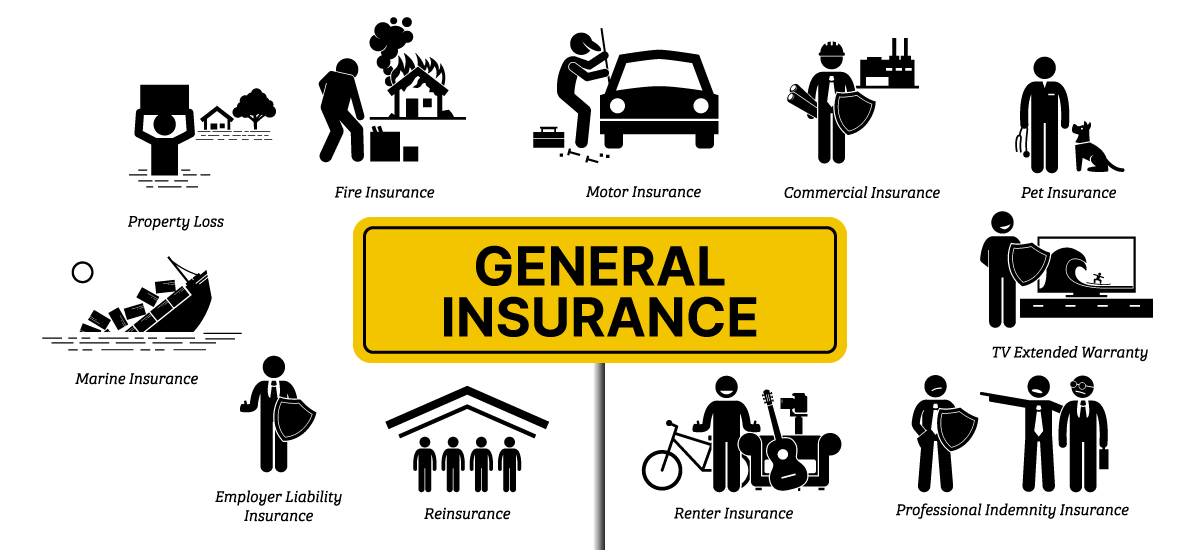

5 ways to save money on your car insurance

Whether you’re buying car insurance or any other type of insurance, there are ways to save money on your premiums. By following these 5 tips, you can save both time and money when it comes to insuring your vehicle or other property. Here’s how…

Types of Car Insurance

When it comes to auto insurance, you have two major types of coverage: Liability: Pays for any damages and injuries that you or your car cause. Collision: Covers damages done to your car in an accident. Comprehensive: Covers anything outside of a collision, including theft or damage caused by weather. Uninsured/Underinsured Motorist: Protects you from drivers who don’t have auto insurance or drivers who do not carry enough liability protection in case they hit you and cause damages. Additional living expenses if you are temporarily displaced from your home due to repairs caused by an accident. Rental Reimbursement Insurance provides funds for renting a car after a collision if your vehicle is not drivable until repaired. Gap Coverage helps pay off your loan balance if your car is totaled in an accident. Other types of car insurance include medical payments, personal injury protection (PIP), and other special add-ons like roadside assistance.

Types of Auto Insurance

If you are looking for new auto insurance, there are four main types of policies: liability only; liability with collision and comprehensive; full coverage (also known as an auto policy or comprehensive policy); and underinsured motorist coverage. Liability: This is a required part of every auto policy in most states and will cover damage that you cause to other cars, people or property. Collision: This covers damage to your vehicle caused by an accident. Comprehensive: This covers all non-collision losses like theft or vandalism, but usually at a higher rate than collision.

How Much Do You Really Need?

Most states require a minimum amount of liability coverage, usually $25,000 for one person and $50,000 for all injuries. The majority of people have even more than that. If you have several assets and someone takes them away, or if you have children who need support later in life and a lot of care now, those are good reasons to consider bumping up your coverage. However, if you are healthy enough that you never go to see a doctor or dentist—even when it’s free because you’re young—you might get by with less. Talk to an agent about what level of coverage is right for you; don’t be afraid to ask questions (and shop around) until you feel comfortable with your decision. Consider asking these questions as a starting point

What Makes Up the Premium?

It’s important to know how you are being charged for coverage. Many drivers see a single number listed for their auto premiums and don’t realize that most auto premiums are made up of four parts: personal injury protection, property damage liability, uninsured motorist and collision/comprehensive. The more risk you have with these coverages, typically, the more you will pay. For example, if you want comprehensive and collision coverage but no personal injury protection or property damage liability – that’s called a binder policy – your premium will be much lower than if you bought comprehensive and collision along with personal injury protection and/or property damage liability. Make sure you understand what is included in your premium before making any decisions about what type of coverage is right for you. If you do not carry certain coverages, your insurer may not provide full protection in an accident. Before buying car insurance, make sure you understand what types of coverages are required by law in your state and whether they make sense for you financially. Some states require certain coverages that other states do not. If so, it might be cheaper to buy only those required by law where you live and buy additional coverage from another insurer if desired when traveling out-of-state.

How Long Should I Keep My Policy?

The length of time you keep a policy depends on several factors, including how much it costs, what kind of coverage you have and how likely you are to make a claim. If, for example, you purchased a policy that cost more than $1,000 and included comprehensive coverage because your vehicle is worth more than $5,000 or was fairly new (which usually means higher replacement costs), then keeping it for less than three years might not be financially smart. On average, about one-third of people who buy policies cancel them within two years. Your insurer will typically let you know when it’s time to renew. This could be as early as 30 days before your policy expires or as late as 15 days after it does. Renewing early gives you more time to shop around if you want to switch insurers, but if you’re happy with your current provider, there’s no need to rush into anything. It’s also important to remember that there may be other options available besides a standard auto insurance policy. For example, if theft isn’t an issue in your area and/or most accidents involve fender benders rather than major damage, then liability-only coverage may work for you—it can lower premiums by up to 25 percent compared with full coverage.